If tax isn’t dealt with on time, HMRC will apply interest and, in some cases, penalties. They are separate charges, calculated differently, and understanding the difference can help reduce the overall cost.

Interest on late-paid tax

HMRC charge interest on most UK taxes, including:

- Income Tax (Self-Assessment)

- Corporation Tax

- VAT

- PAYE and National Insurance

- Capital Gains Tax

- CIS

- Inheritance Tax (on unpaid balances)

This rate is variable and linked to the Bank of England base rate + 2.5%. So, when interest rates go up and down, so do the rates HMRC charge. The current late-payment interest rate is 7.75%.

HMRC interest rates for late and early payments – GOV.UK

If you haven’t paid a tax liability by the due date, it is more than likely going to start accruing interest. Interest is charged from the day after the tax was due and calculated daily.

HMRC calculate the amount using simple interest, meaning interest is only charged on the original amount and not on any interest already added (i.e. interest does not compound).

Interest is payable even where a Time to Pay arrangement is in place.

If you pay your tax ahead of time, HMRC will pay you interest on the amount they have been holding. The catch is that this is only paid at the bank of England base rate minus 1%. The current repayment rate is 2.75%.

Payments for late filing and late payment

Penalties are separate from interest and depend on what deadline has been missed.

Late filing penalties apply where a return is filed late, regardless of whether tax is owed. This includes Self-Assessment returns, VAT returns, Corporation Tax returns and CIS & PAYE submissions.

Late payment penalties can also apply where tax is paid late, even if the return was filed on time. These usually increase the longer the tax remains unpaid, but HMRC can use their discretion if a penalty is appealed.

You may also receive a penalty for failing to register for the correct taxes at the correct time.

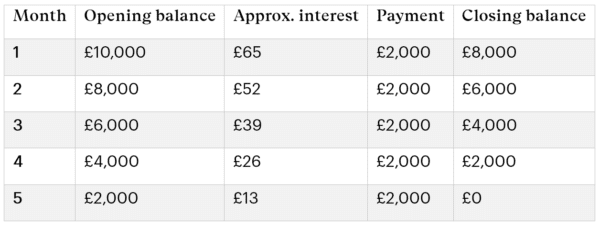

Example:

If cash flow is tight, it is often better to speak to HMRC early and agree a Time to Pay arrangement or making an application online.

Interest will still apply but late payment penalties can often be reduced or avoided if agreed promptly and the overall cost is usually lower than waiting and paying in one lump sum later.

In this example, we have used a £10,000 tax bill paid over a period of 5 months.

Interest rate: 7.75%

Repayment plan: £2,000 per month

Interest calculated daily on the outstanding balance

As the balance reduces, the interest reduces too.

Total interest paid is approximately £195

By paying the tax down gradually, the interest cost is significantly lower than leaving the full balance unpaid for several months.

Interest is automatic and unavoidable when tax is paid late but penalties depend on what has been missed and how long it takes to resolve.

Speaking with HMRC, filing on time and structuring payments can reduce the cost, especially at today’s interest rates.

HMRC interest rates could work out to be more favourable that other borrowing, alongside the interest not being compounded, so agreeing a payment plan might be the best way to structure repayment of your liabilities if you find yourself with cashflow challenges.

For other help with unpaid tax or cashflow concerns: Get free debt advice – GOV.UK

As always, we’re here and happy help!

Give us a call on 01872 267 267, email us [email protected], or message us on WhatsApp 0777 49 39 111

Get notified of our latest blog posts, along with lots of other good stuff, over on our socials: