From 1st April 2026, the National Living Wage increases again. And if you employ people, at any level, this one is worth paying attention to.

Here’s what that means in practice, and what you need to do about it.

From 1st April 2026:

Increases to the National Minimum Wage (NMW), National Living Wage (NLW) and Real Living Wage (RLW).

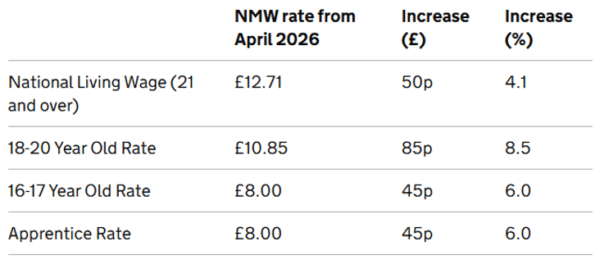

- The NMW applies to employees age 18-20. This is currently £10.00 per hour.

- The NLW is for employees age 21 and over, this is currently £12.21 per hour (it increased from £11.44 on 1st April 2025)

- Both the NMW & NLW are a legal requirement for the minimum hourly rate and employee can receive.

This change comes into force on 1st April 2026 but the tax year ends on 5th April 2026 so if you pay your employees weekly, the payroll for the week commencing 30th March 2026 will contain the change midweek.

NMW & NLW increases:

The Real Living Wage is not a mandatory requirement but has become part of a wider movement to pay an hourly wage that has been calculated against everyday living costs. This amount is increasing from £12.60 to £13.45 and applies to all employees over the age of 18 (excluding apprentices in their first year).

If you are a Real Living Wage accredited employer, you have to implement the latest increase by 1st May 2026.

The costs for an employer paying either NLW or RLW based on an employee working 40 hours per week have been summarised below:

This latest update takes a basic salary to £26,436.80 plus employer NI & Pensions. The total costs to the employer will be £30,258.22.

The same cost on 31st March 2025 was £26,349.79. This means employers have seen cost increases of £3,908.43 or 15% in a 12-month period.

Of the increase: £2,639.94 is a benefit to the employee and £1,268.49 is contribution to HMRC.

In the last 5 years, the cost to an employer for an employee paid National Living Wage has increased by 62%. In 21/22 it was a total cost of £18,734.12 up to the latest figures of £30,258.22. (only 65% of this increase benefits the employee)

In the same 5-year period, the personal allowance has not increased. For employees, this has meant a change from 28% of earnings being subject to tax in 2022 to 52% in 2026. This is fiscal drag. And the freeze of the personal allowance until 2031 is likely to see this figure reach 61% in 4 years’ time and a forecasted NLW cost to employers of £37,000.

Fiscal drag occurs across the entire earnings landscape and puts pressure on individuals who are earning more but taking home less.

Actions:

- Ensure you know which employees fall under this latest update.

- Calculate the cost across your business.

- Based on your Gross Profit margins, work out the additional revenue needed to meet this cost.

As always, if you have questions, we’re here and always happy to help. But, rest assured, we’re on top of these changes and looking out for you.

As ever, we’ve got this

Get notified of our latest blog posts, along with lots of other good stuff, over on our socials: